Evergrande – A Potential Global Contagion. Will It Impact Crypto?

There have been major headlines, and a lot of talk and speculation concerning the Chinese developer, the Evergrande Group, and its demise and potential collapse it is facing. Could we be on the verge of another Lehman Brothers moment? An uncontrolled default of the Evergrande group could lead to a credit crunch, implicating all financial markets globally. But what about crypto?

Chinese Property Bubble

Before we discuss Evergrande, let’s look at the Chinese property bubble. It has, after all, provided the ingredients for this company to become so systemic. To say that the Chinese property market is in a bubble is an understatement. It's been so hot recently that off-plan units sell out online in minutes.

For example, in March of last year, 288 apartments in a new Shenzhen development sold out in less than eight minutes. A few days later, an additional four hundred units sold out in record time.

People are legitimately willing to fork out upwards of $100,000 immediately just to have the opportunity to buy a property 2 to 3 years from now. One of the main reasons the Chinese property market has been exploding at such a pace is that property is seen as one of the primary forms of investment in the country.

When compared to their western counterparts, Chinese citizens own more property than they own bonds or stock. In China, at least 96% of urban households own at least one home. In the US, however, that number is closer to 65%.

Furthermore, statistics reveal that $900 billion a year was invested into the property market at the peak of the US property boom. Currently, there is $1.4 trillion being invested in Chinese property. However, in recent years, buying property in China has been more about speculation than investing.

They've been investing in property mainly because of their belief that prices will always go up. This belief, of course, is a self-fulfilling prophecy that we've seen on many occasions, including back in the 2008 subprime mortgage crisis.

The graph below shows the annual residential real estate investment in China versus in the US. As indicated, the Chinese bubble has grown and grown. Even the 2008 financial crisis did nothing to that demand, and it kept on climbing throughout.

However, much like 2008, this Chinese property bubble is not being built on savings. There is a lot of debt being taken out to buy these homes. For example, from 2010 to 2019, China accounted for 57% of the total increase in household borrowing compared to the US, which only accounted for 19%.

It's not only the fact that this debt-fueled property bubble is systemically dangerous, but it's also leading to massive increases in the cost of living. Interestingly, in an upmarket area of Tianjin with a population of about 15 million, apartments cost around $836 per square foot, which is around the exact cost of the most expensive areas in other parts of the world, where the disposable income is seven times more than in Tianjin.

This property boom has not gone unnoticed by the Chinese Communist Party, and it has become increasingly worried about this speculation. General Secretary of the CCP, Xi Jinping, stated that “housing is for living in, not for speculation.” But they're in a catch-22 situation here; Given that so many people have their net worth tied up in housing, if the government were to try and deflate that bubble, it could lead to social unrest, and that is not something you’d want in a one-party state or anywhere else, for that matter.

It's kind of a weird symbiosis where the CCP is happy to let the property market continue its growth provided it keeps the people happy, which has been the case. But eventually, as has happened with any number of asset bubbles in the past, when the ingredients that first drove the bubble and are no longer there, you have an epic crash.

Who And What Is Evergrande?

Evergrande is one of the largest property developers in China. It was established in 1996 in the southern city of Guangzhou and has grown at a breakneck pace ever since. Its founder, Hui Ka Yan, was at one point the richest man in China as he steered Evergrande through that Chinese property boom. In 2009 the company did an IPO on the Hong Kong Stock Exchange and raised almost $1 billion.

The firm owns more than 1,300 projects in over 280 cities across China to give you an idea of just how prominent this developer is. It's also a massive employer in the country. It employs over 200,000 people, and if we include all the people who work on its projects as contractors or subcontractors, that figure expands to over 3.8 million.

But the company had ambitious goals and always wanted to expand beyond just property. It decided that it wanted to diversify into several different sectors and business units heavily. In some cases, these were as far from its core competency as they could be and included building electric cars, food and beverage businesses, bottled water, and dairy products.

In 2010, the company bought a soccer team and also built a soccer school. It also had aspirations of building a 1.7 billion dollar soccer stadium in Guangzhou, where this team could play. Evergrande has recently laid out ambitions to build museums, theme parks, a health chain, and even into the financial services business by offering people wealth products.

Image by The Civil Engineer

These lofty ideas to branch out from residential real estate would have been quite feasible if Evergrande could fully fund this expansion, but the sad reality is that the bulk of this expansion has come due to piles and piles of debt. $300 billion, to be exact.

Building Purely On Debt

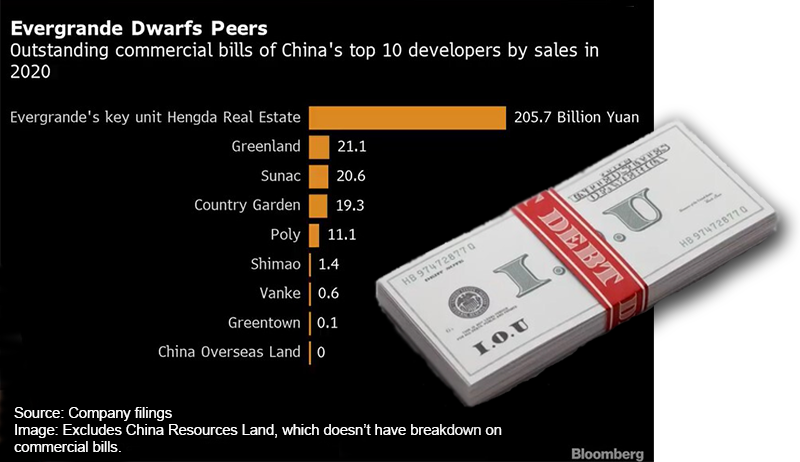

This debt burden has made Evergrande the most indebted property developer globally, and this sobering fact has come back to bite the company. In its rapid expansion over the last few years, Evergrande has taken on all forms of debt. These include the likes of bank loans, bonds, and international dollar bonds.

However, one of the most common forms of debt that it's taken on is commercial paper. To clarify, this is shorter-term unsecured debt such as IOUs and other payables. It's an interest-bearing note that large banks or corporations typically issue to meet short-term financial obligations.

Evergrande issued this commercial paper to all suppliers and contractors who worked on its projects. It was given as a substitute for cash and viewed as very secure. So secure that these very suppliers and subcontractors used the Evergrande commercial paper as a method to pay their suppliers, Etc.

So, Evergrande commercial paper was essentially transformed into a quasi currency that people viewed as legitimate, despite being literally unsecured debt. This practice of using commercial paper to fund operations is not exclusive to Evergrande, but it has been one of the most prolific issuers.

Then when it comes to more traditional forms of debt, Evergrande has taken out billions in bank loans from many Chinese Banks. Last year, Evergrande reported total bank and other borrowings of around $107.4 billion. This debt would have been all well and good if Evergrande had been able to pay it back.

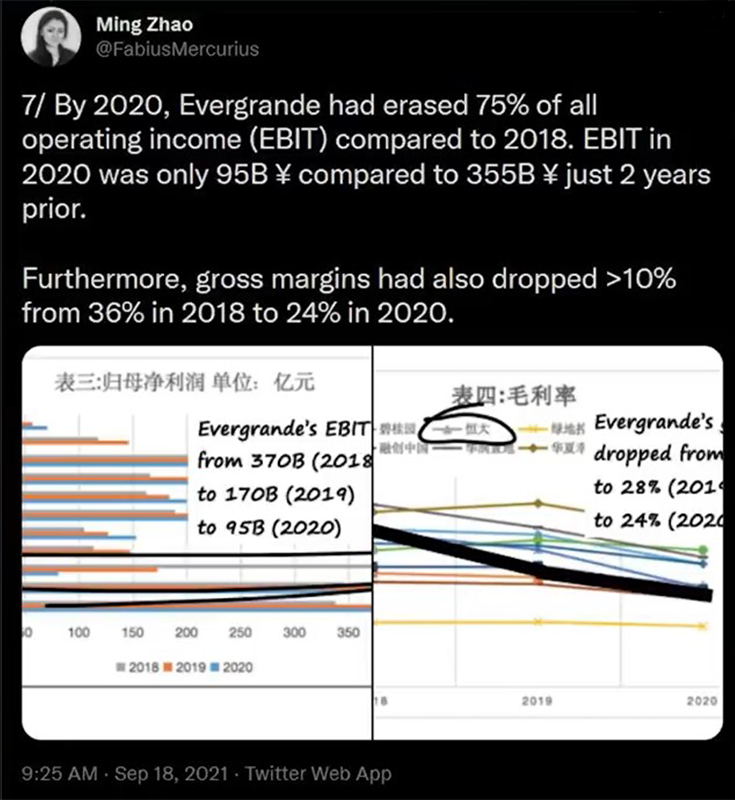

However, Evergrande’s bottom line has been deteriorating over the past couple of years. In 2020, Evergrande’s operating income was down 75% two years prior, plus there was also a fall in gross margin. The chart below shows how precipitous that fall in revenue has been, courtesy of Ming Zhou on Twitter.

So what all that means is that Evergrande has even less below-the-line income to pay interest on its outstanding debt, let alone the principle. This realization has come to a head, and the company publicly admitted, a few months ago, that it may not be able to service all of its debt. Banks in China have started freezing Evergrande deposits to keep some collateral for paying back these loans.

Default Is On The Cards

Of course, the international financial markets have taken notice. S&P has downgraded Evergrande’s dollar bonds from CCC to CC, with a negative outlook, and raised the chances of a debt restructuring or default. Fitch also downgraded Evergrande and its subsidiaries.

The markets have also reacted as bonds trading near par back in May are now trading at close to 30 cents on the dollar. This shows that these bond investors think that a default is on the cards. It's not just the debt market that's taking a hit, though. Evergrande shares have been on a sustained decline over the past few months, and they're already down 80% this year.

Notably, Evergrande has not only issued a great deal of commercial paper to its suppliers and lenders. It has also taken money in deposits from close to 1.5 million people. These are people who put down these deposits hoping that they would one day buy some property from the developer.

This begs the question; if this company is so essential to the Chinese real estate sector and it's teetering on the brink, why doesn't the Chinese government bail it out? After all, they are a centrally planned economy, and they have the final say.

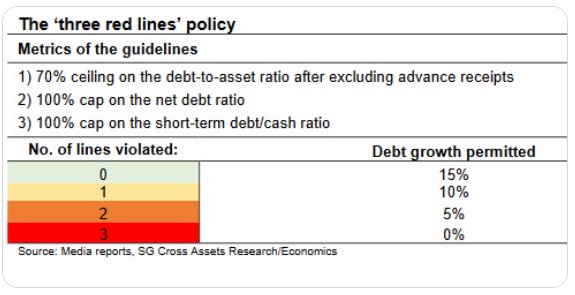

Answer; the Chinese government has taken a hard line on leverage in the property development sector. A few years ago, it came out with directives to limit debt. These have become known as the Three Red Lines.

These are cash on hand, the value of their assets, and equity in their businesses. Banks are required to limit real estate lending to 40% of their total under rules taking effect in January. The CCP would not want to create a moral hazard by bailing out Evergrande. If anything, it would more than likely want to make an example of the developer.

So what all this means is that a default is not only likely but inevitable. In the case of the behemoth that Evergrande is, it may get ugly because of the contagion effect this could have across China's property sector and include its global credit markets. So there is a real risk that it won’t be contained within China; it will spread to the rest of the world, much like the 2008 credit crunch did.

The counterparties that are at risk and Evergrande’s liabilities involve more than 128 banks and over 121 non-banking institutions, according to the letter Evergrande sent to the government late last year. Depending on how much exposure these counterparties have, there could come a situation in which they would themselves become too hot to touch.

Let's also not forget about how much of that Evergrande commercial paper is out there. It's not well-tracked, and it has helped develop an entire quasi shadow banking system of suppliers, buyers, contractors, and counterparties.

All of these folks have been using Evergrande paper as if it was as good as gold. There's no way a company as big as Evergrande could go bankrupt, right?

Now, this fear of default could also spread to the other indebted property developers. Banks may become concerned about their ability to service their debts, and their commercial paper and bonds would also become toxic.

Even if this is not the immediate result, you have a perverse situation where even the action of Evergrande trying to make good on its debt can precipitate a worse debt problem. This is because to raise funds, to settle its debt, it will have to sell assets.

The overwhelming majority of Evergrande’s assets are property. If there is a fire sale of its properties, this could lead to a property crash and hurt everyone in the country. It would send all the property developers in the country into further, negative territory and damage the savings of all those Chinese who bet on the market. It creates a spiral where the collateral backing debt is falling in value, making everyone more indebted.

Impact On International Markets – Global Contagion

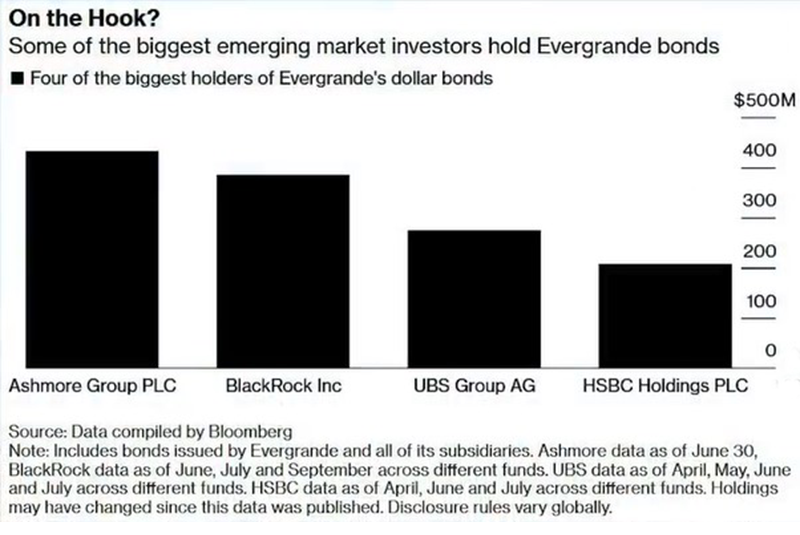

This has a significant impact on international markets as there are a lot of holders of Evergrande’s debt offshore. These include asset managers, international bond funds, and other corporations.

For example, a large bond fund called Ashmore Group, based in London, has over 400 million dollars worth of Evergrande bonds. Other asset managers that have exposure include BlackRock Inc., UBS Group, and HSBC Holdings. Both BlackRock and HSBC boosted their Holdings of Evergrande debt as recently as August.

And these are only their International bonds. When it comes to the mountains of Evergrande commercial paper, no one really knows. This is a lot harder to track as these assets are not standardized securities like bonds.

Moreover, what happens if the contagion spreads to the rest of the Chinese developers, banks, and companies? What happens if their debt cannot be paid? The risk of contagion in the Chinese property and credit markets could wreck the portfolios of these managers that hold their debt. And that's just the debt side.

We should not forget that these Chinese developers, banks, and companies have publicly traded equity on International markets such as the Hang Seng or Shanghai stock exchanges. If these were to tank as they did with Evergrande, it could further hurt international portfolios.

Impact On The Cryptocurrency Market

What about the crypto market? In times of market stress, we’ve learned that Bitcoin and other cryptocurrencies assets have a pretty strong correlation with equity markets and are not entirely isolated from what’s happening on the global macro front. We saw this play out last year during the covid-inspired crash. We also saw it happen numerous times over the past few months with concerns about potential Fed tampering.

It could be that large fund asset managers and institutions based out in Asia may have to sell their Bitcoin holdings to cover the losses that they hold in shares or debt of these developers. Or maybe the situation in which retail investors in China have to sell their crypto holdings to settle their debt. Even though the Chinese government has been trying to prevent its citizens from holding crypto, it hasn't fully succeeded as Bitcoin traders in China still wield enormous influence.

Bitcoin is an asset that faces the same risks in the short term from global financial contagion.

Image and related Article by Cointelegraph.com

However, one other factor unique to the crypto markets and has been drawn into the Evergrande saga is Tether. There are concerns that the controversial stable coin issuer, Tether, could be quite exposed to Evergrande. These suspicions have arisen due to a disclosure that the company hoped would temper the FUD and not add to it.

That disclosure is the attestation report.pdf issued by Moore Cayman a few months ago, giving a breakdown of the reserves backing up USDT, stating 50% of its reserves were held in commercial paper and certificates of deposit. That equates to $30 billion.

One question comes to mind: Why does Tether have so much commercial paper? Well, there are two possible reasons. One is that it likes to earn interest on this commercial paper, and the other is that there are very few banks that would be willing to hold $30 billion in cash and cash equivalents or Tether.

The question that many have been asking is whether Tether has any Evergrande commercial paper. Ever since this speculation has come to light, Tether has emphatically denied holding any Evergrande commercial paper.

If it were the case, it would mean that the reserves are not fully backed because all that commercial paper would be worth a lot less. Even if it were only a tiny component of the commercial paper, the knowledge that USDT is not 100% backed by assets would create a great deal of uncertainty around holding USDT.

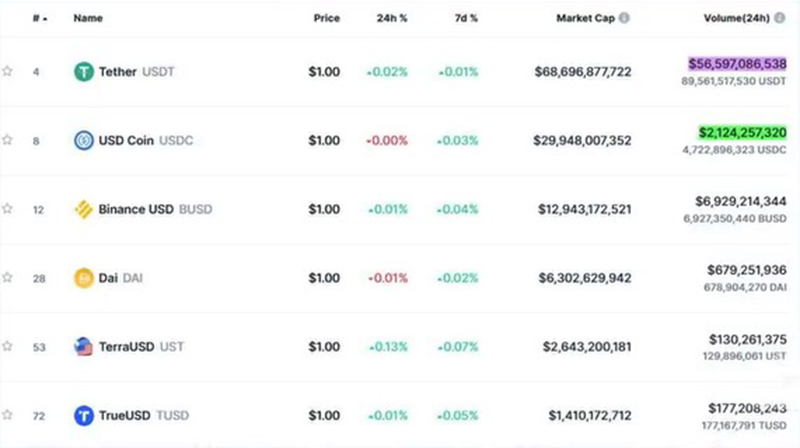

So, why does this matter for the crypto markets? Well, because Tether remains one of the essential components for Bitcoin liquidity. On many offshore exchanges, it is the stable coin pairing of choice as indicated on Coinmarketcap. USDT trading volume stands at $56 billion per day. It is 28X more than the next-in-line USDC shown on the chart below.

Image CoinMarketCap

So, quite simply, if there is a crisis of confidence in Tether, this trading volume could dry up. People would be reluctant to use Tether to trade, creating a systemic liquidity crisis in crypto.

The goal of this article is not to cause FUD. It’s to create awareness of a risk that is not being adequately considered. Whether we see a full-blown financial crisis due to an Evergrande default is not clear as yet. It all depends on whether the Chinese government will come to its aid. A complete bailout by the Chinese government is the only thing that could help stave off the contagion.

But on the other hand, if the CCP does assist, it creates a perverse incentive where developers will think that the rules don't apply to them when they binge on debt. This is precisely what happened on Wall Street in the wake of the financial crisis. So right now, the CCP is stuck between a rock and a hard place.

Optimism Remains Prevalent In The Crypto Markets

Despite all of the short- to medium-term risks an Evergrande default poses, there is good reason to remain optimistic about crypto in the long run. Fundamentally, nothing has changed, and external factors are beyond our control. Even if there is a situation that snares Tether, it could help to serve the long-term stability of the crypto markets.

Tether Inc. has been at the center of controversy and FUD for years and is reportedly not particularly transparent. Many crypto enthusiasts would love to move to a reality where this FUD is no longer in the picture. If ever there was a crisis in confidence of Tether, it could lead to a legion of long-term hodlers. People would be reluctant to convert to stable coins, including USDC.

Either that or they would convert their BTC holdings into other cryptocurrencies, which benefits the ecosystem holistically. The future is still bright for many cryptocurrencies with purpose and utility. Ultimately, this could lead to a new financial operating system and be needed to sidestep any debt-based or quasi currency.

Resources: Coin Bureau

Also published on Before It’s News

https://beforeitsnews.com/financial-markets/2021/10/evergrande-a-potential-global-contagion-will-it-impact-crypto-3385095.html

Bruce Jacobs